ShreyasSomnathe

Quantitative Researcher & Trader building ML-driven systematic strategies for global energy and index futures

Sharpe Ratio

Live Strategies

Projects

What I've Built

Production trading systems, research platforms, and quantitative infrastructure for energy futures markets

Crude Oil Forward Curve ML Trading System

Production Trading System

Production ML system for crude calendar spread trading using PCA of forward curve (level/slope/curvature), VAR for lead-lag relationships, and Kalman filtering for regime detection. Integrated EIA, FRED, Cushing inventory, and refinery data across 3 live strategies with FastAPI execution and PostgreSQL.

sharpe

3.4

strategies

3 Live

assets

Energy Futures

Quantitative Trading Analysis Engine

Research Platform

Python platform for high-frequency CL futures analysis (1.44M rows, 842 patterns) with Shannon/Renyi/Tsallis entropy, chaos theory (Lyapunov exponents, Grassberger-Procaccia), Markov chain models, and network topology analysis. Risk frameworks: Kelly Criterion, VaR/CVaR, Sharpe optimization.

rows

1.44M

patterns

842

methods

10+

assets

CL Futures

Energy Trading Infrastructure & Dashboard

Full-Stack Platform

Full-stack trading infrastructure with Python strategy engine (mean-reversion, momentum, volume breakout), FastAPI + WebSocket backend, and React dashboard with live P&L, order blotter, TT API integration, strategy metrics, and system monitoring.

strategies

3 Types

latency

Sub-sec

monitoring

Live

api

TT API

CL Intraday Spread Research

Quantitative Research

18.3M minute-level bars across WTI crude oil forward curve. 37 hypotheses tested with institutional-grade methodology. Discovered bifurcated market structure and butterfly reversion strategy with abundant signal capacity.

bars

18.3M

hypotheses

37

signals

7.4K/yr

methods

12+

Research

CL Intraday Forward Curve Microstructure

How does information propagate across the crude oil forward curve within a single trading day? This framework analyzes minute-level dynamics across WTI outright + calendar spreads, revealing a bifurcated information structure with exploitable divergences.

Bifurcated Information Structure

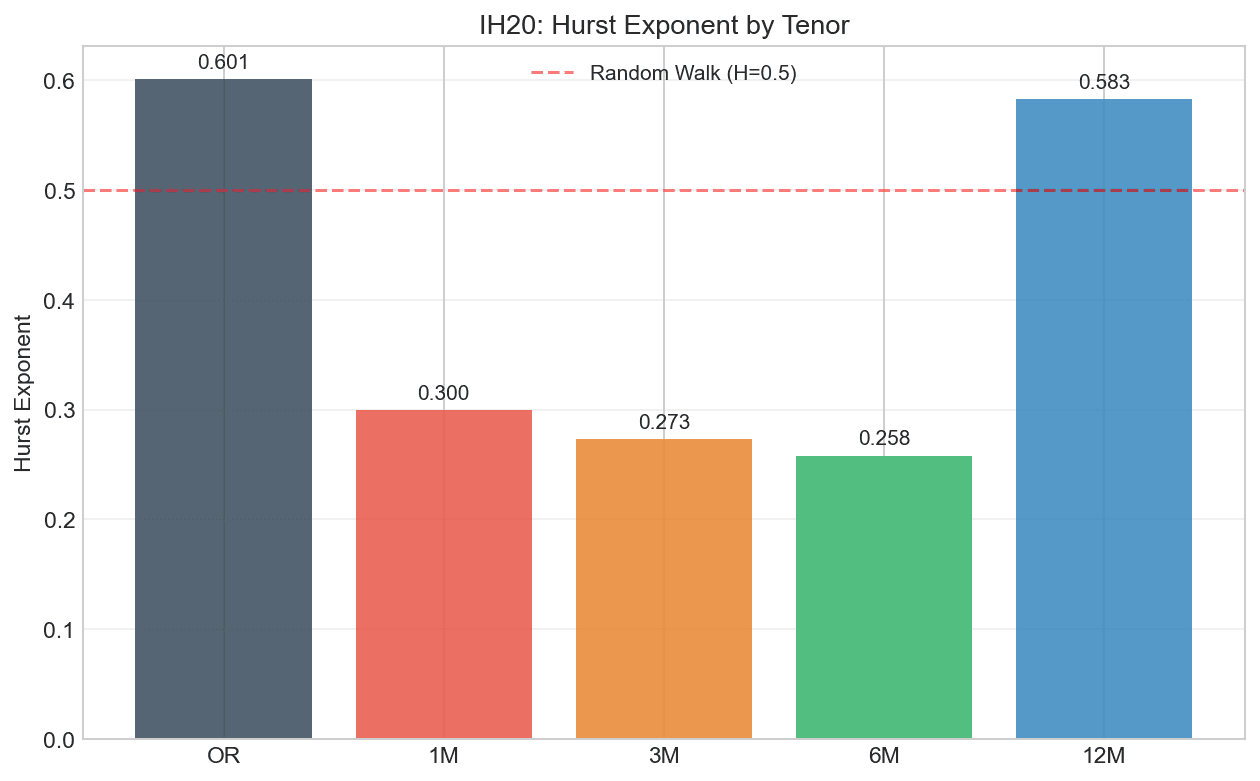

Hurst < 0.5 vs > 0.5

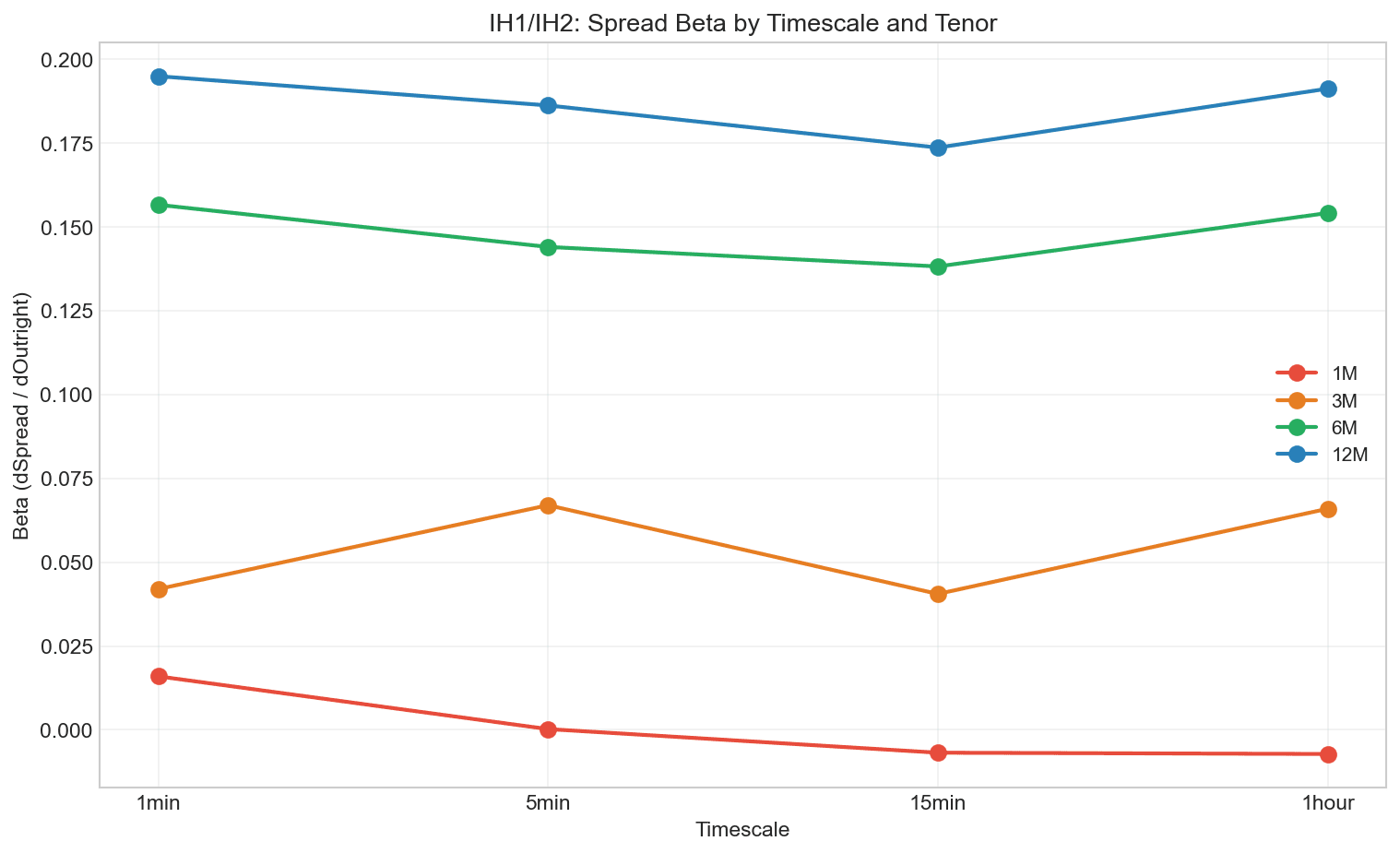

Beta Magnitude Collapse

Daily 2.5 → Intraday 0.02

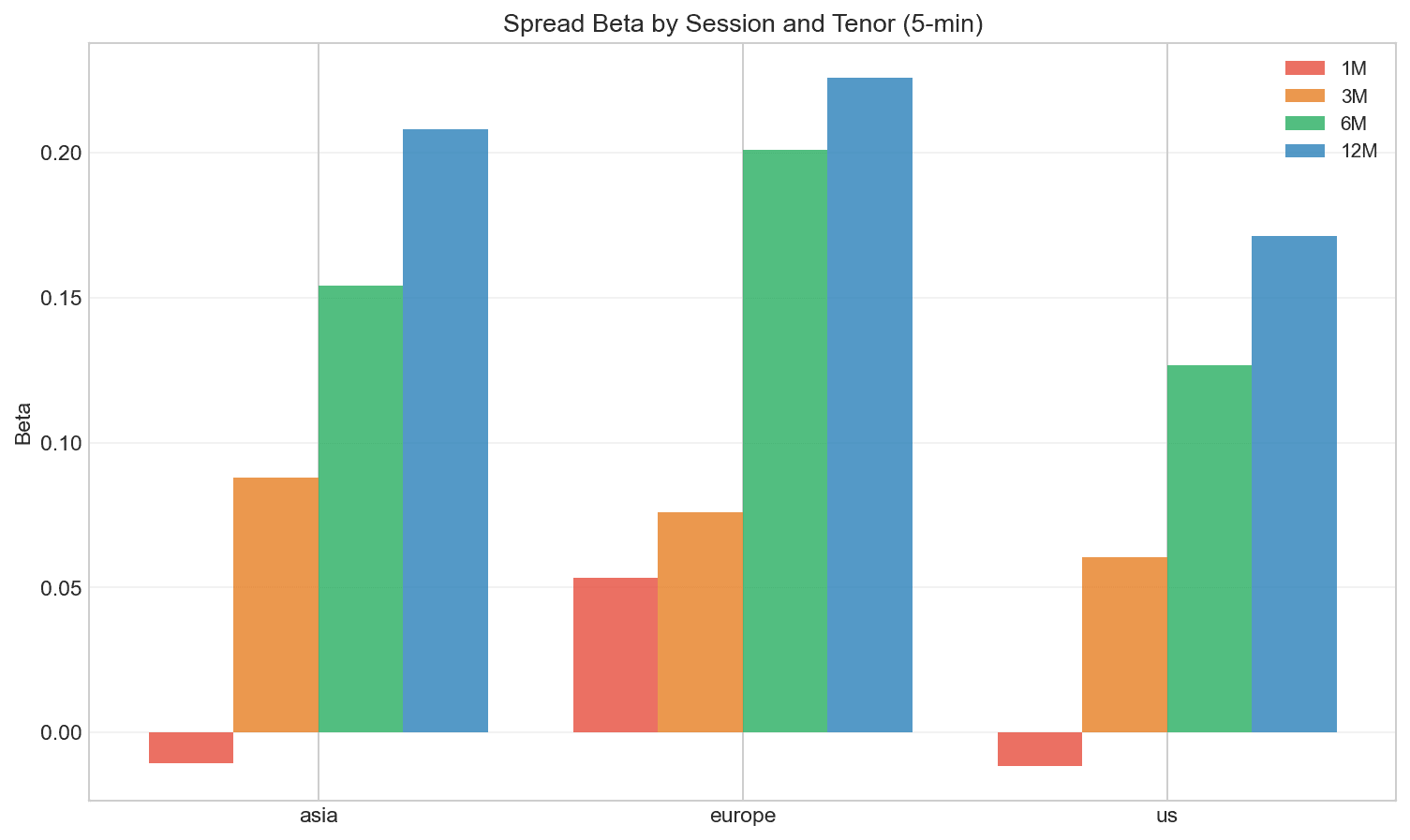

Session Energy Cycles

63-90% Compression Rate

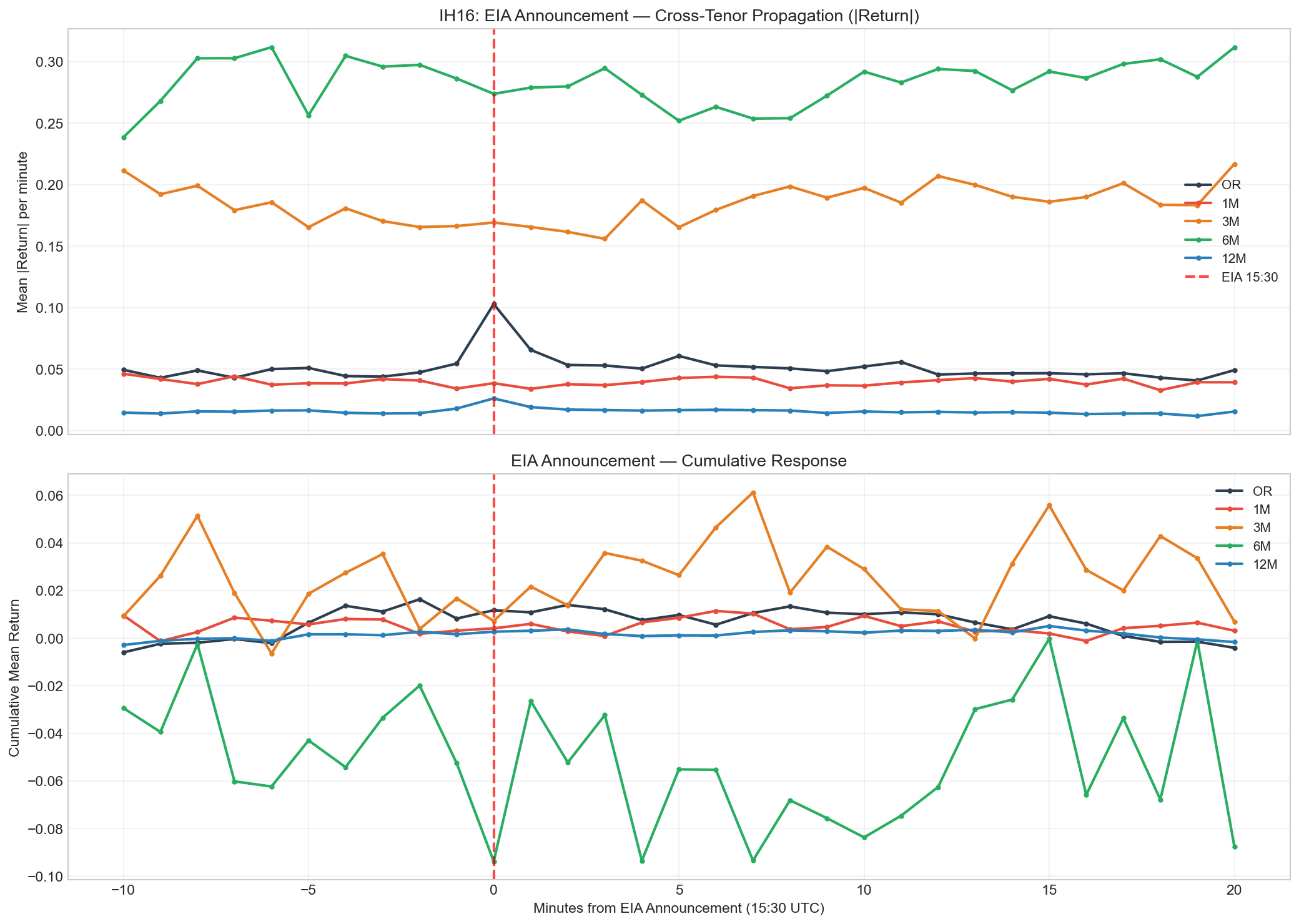

EIA Paradox

Amplify OR 1.48x, Suppress 1M 0.74x

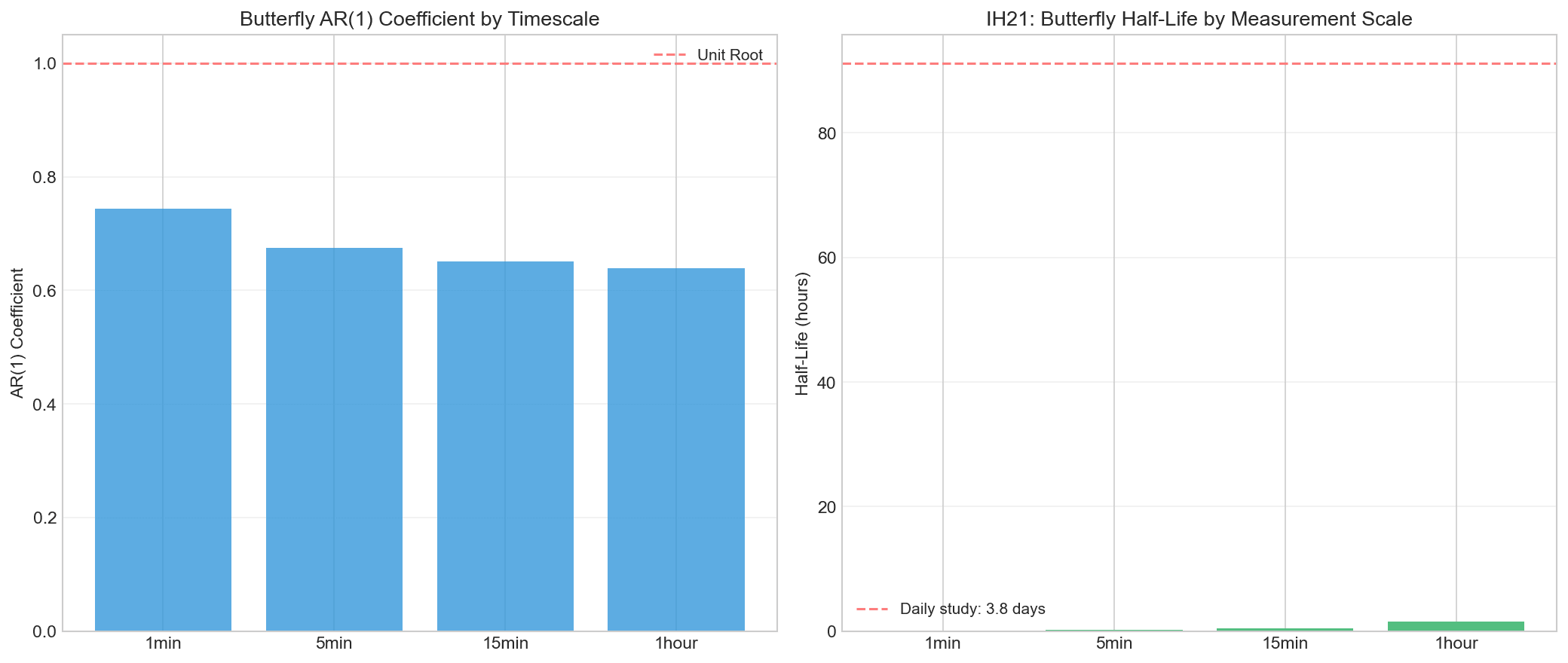

Butterfly Reversion

2.3 min half-life (2,400x faster)

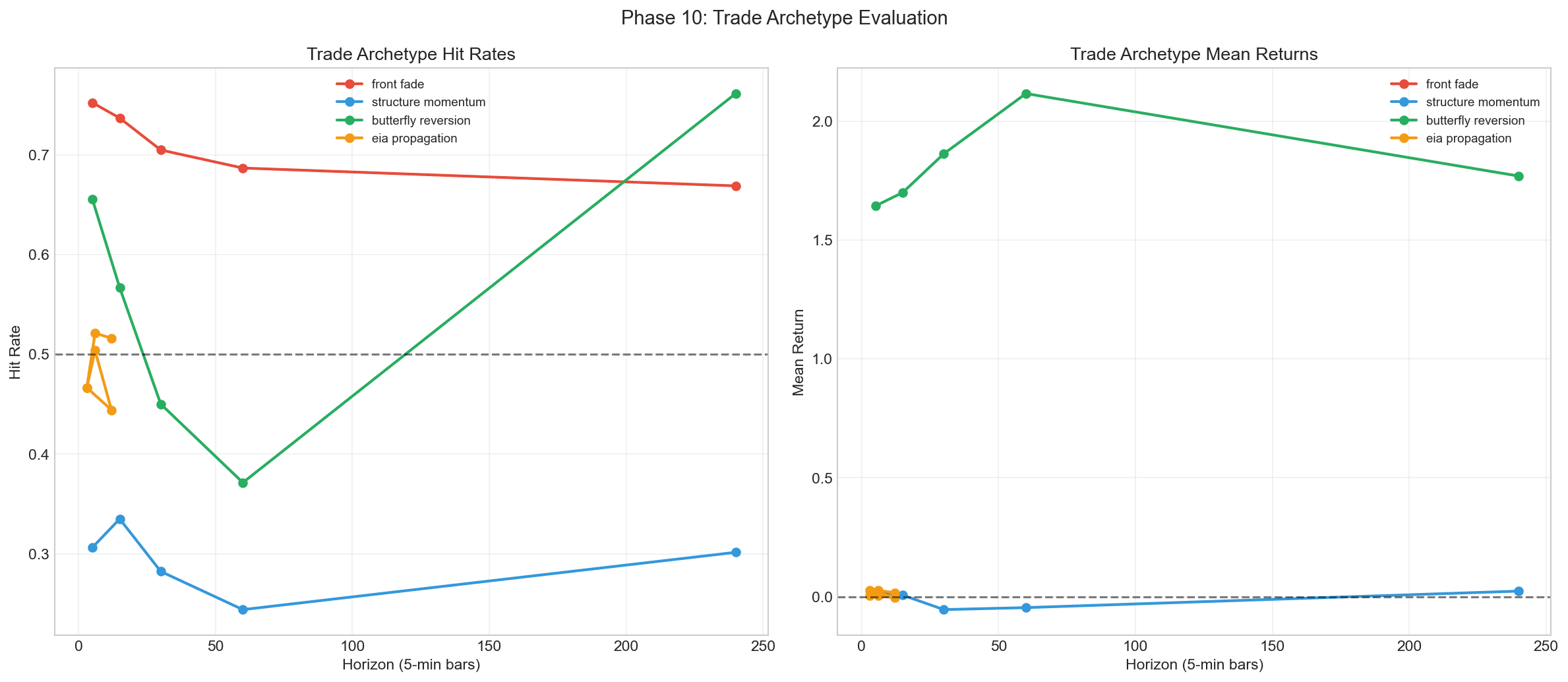

Trade Archetype Winner

7,400 signals/yr | Top Archetype

Quantitative Methods

Visualizations

22 plotsBeta Analysis

4 plotsBeta Convergence by Timescale

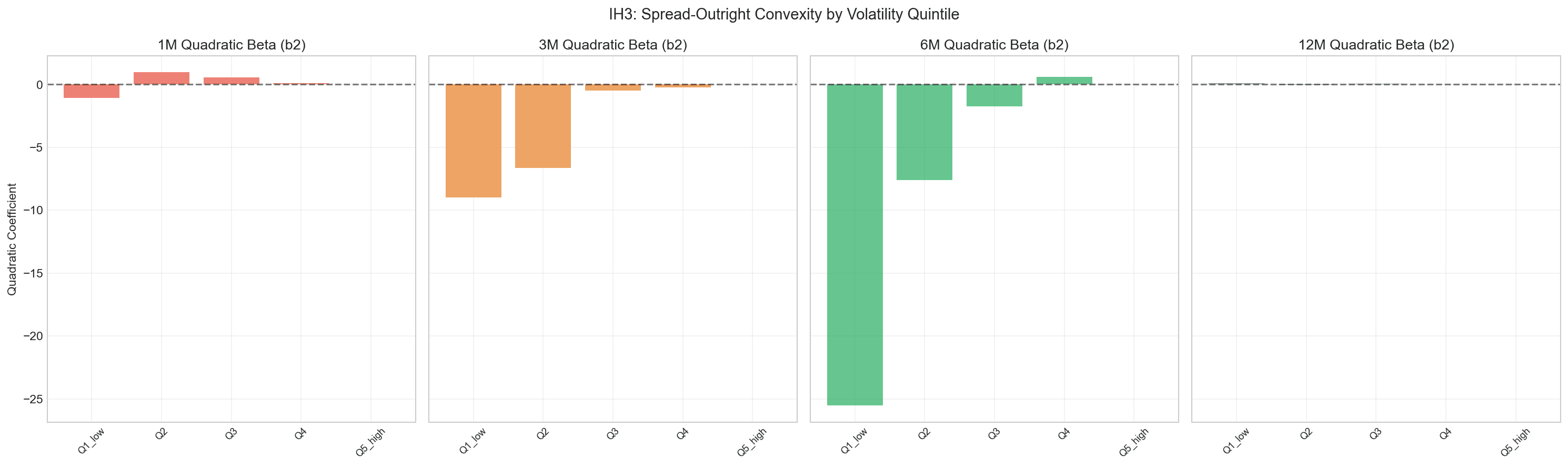

Nonlinear Beta by Volatility Quintile

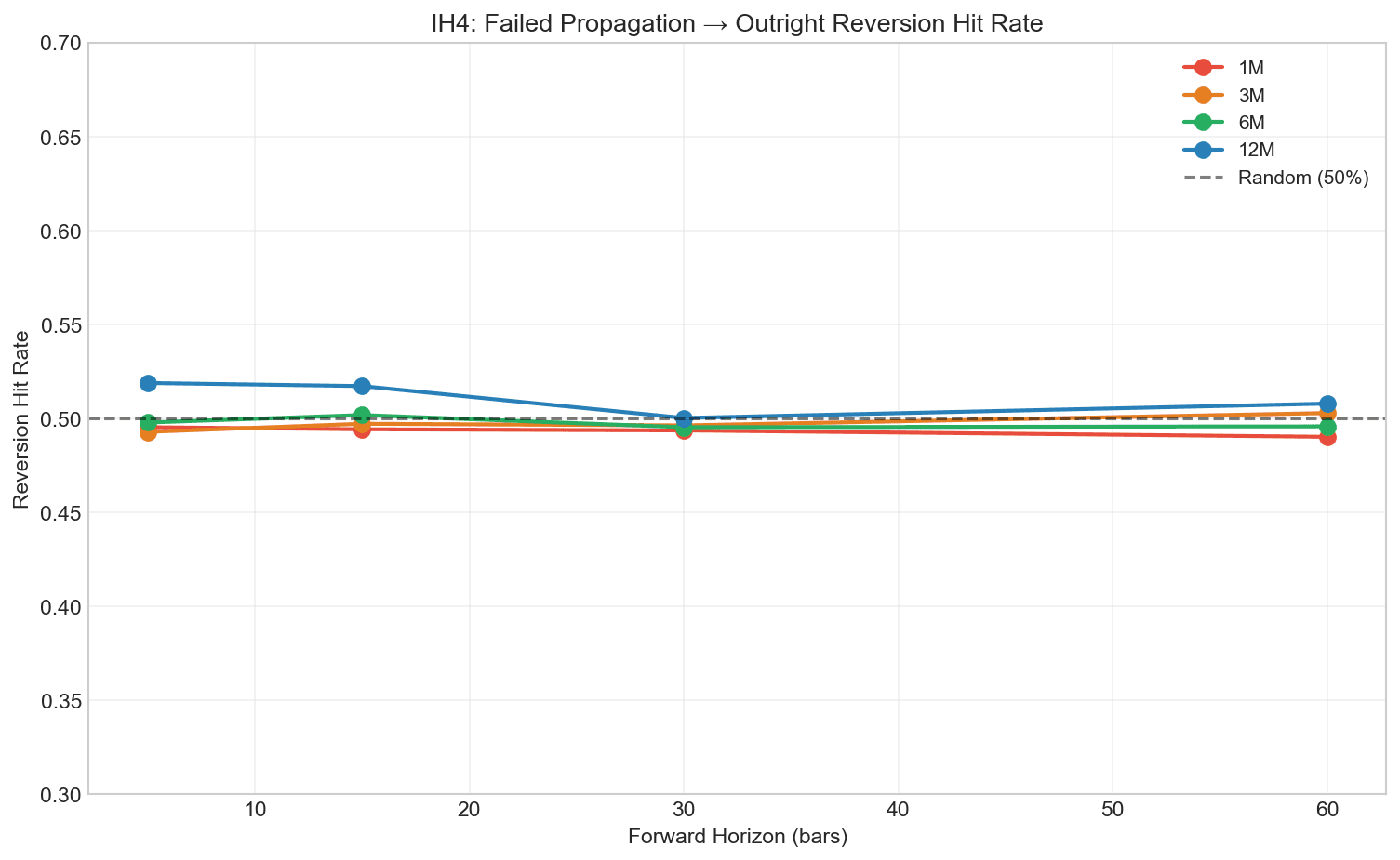

Failed Propagation Hit Rates

Session-Conditional Beta

Lead-Lag

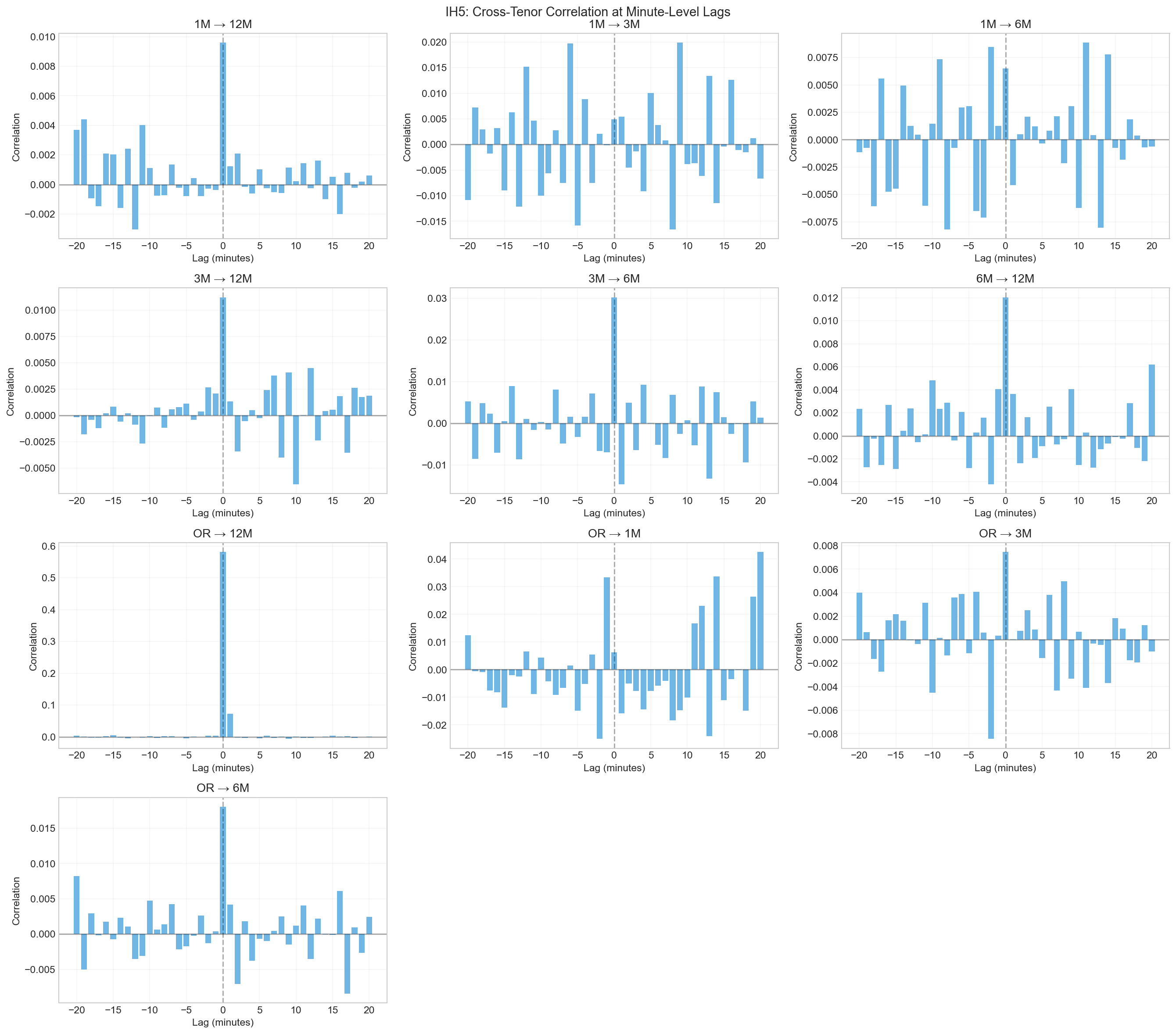

2 plotsCross-Tenor Correlation at Minute Lags

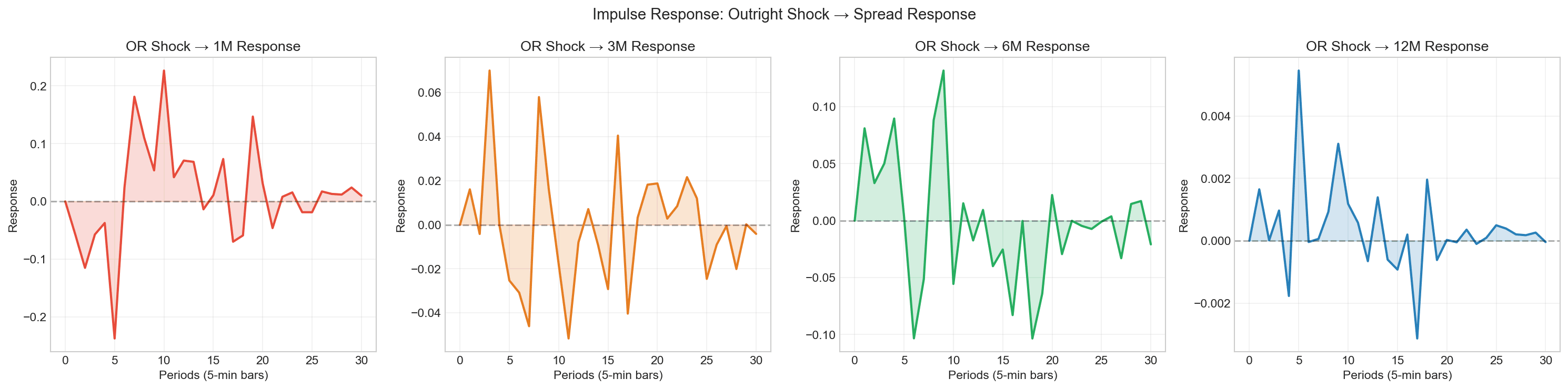

VAR Impulse Response Functions

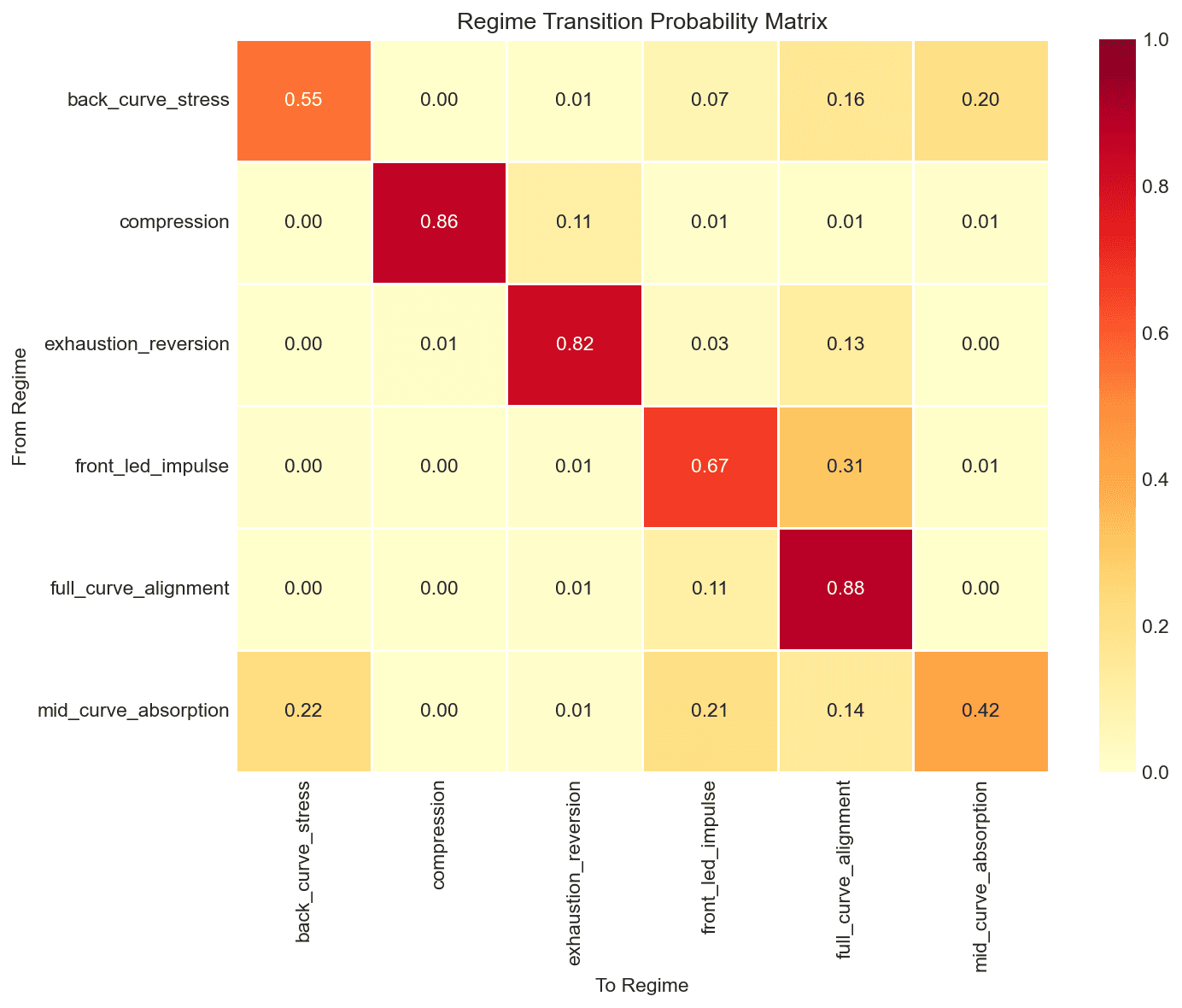

Regimes

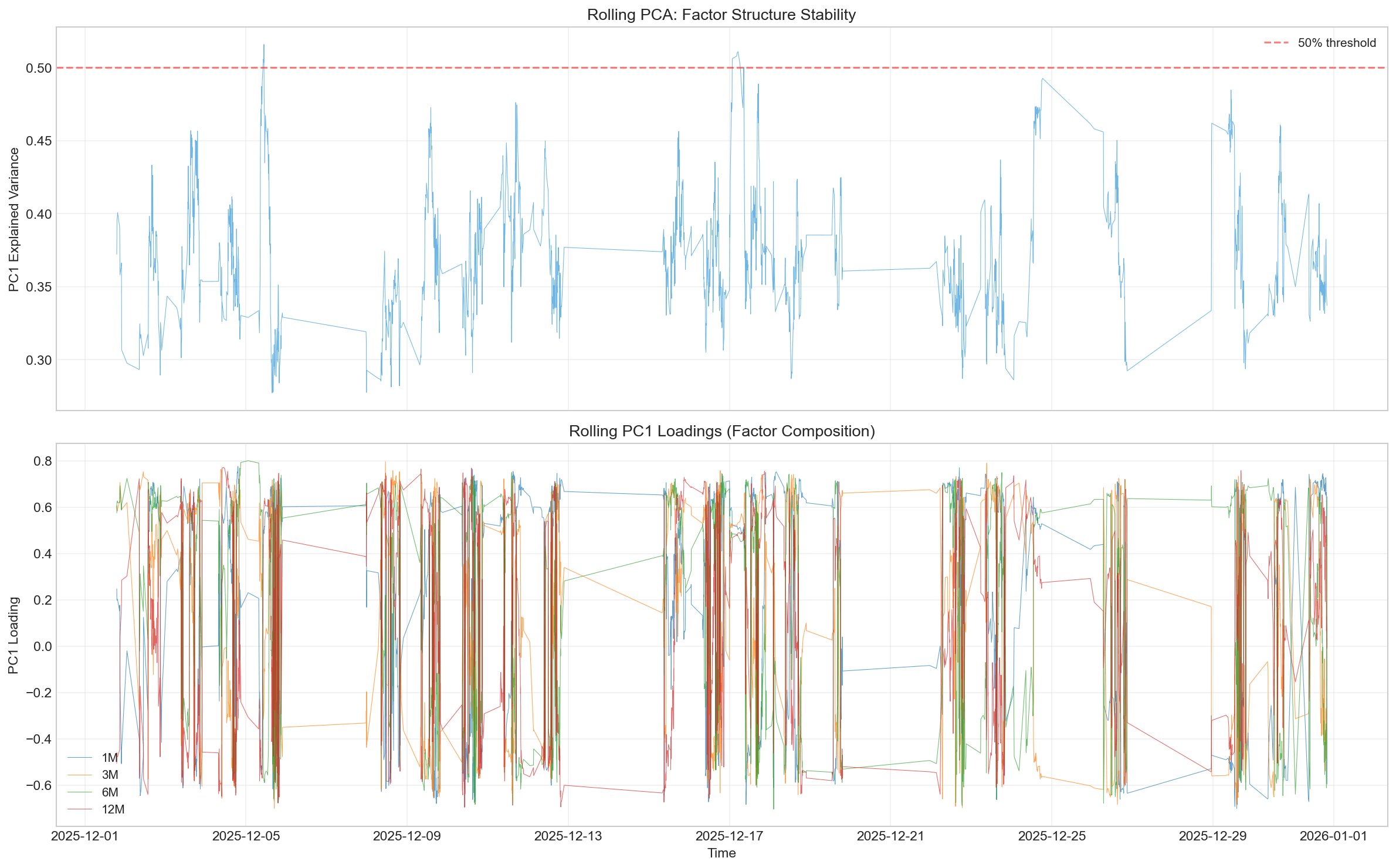

3 plotsRolling PCA Explained Variance

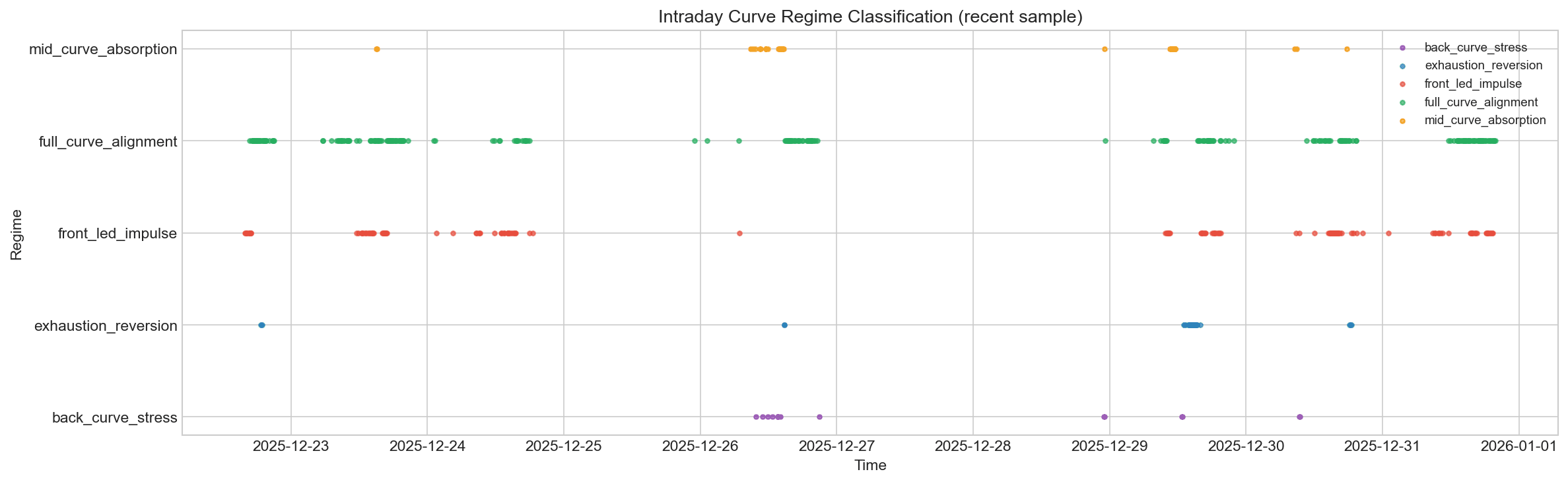

Regime Classification Timeline

Regime Transition Probabilities

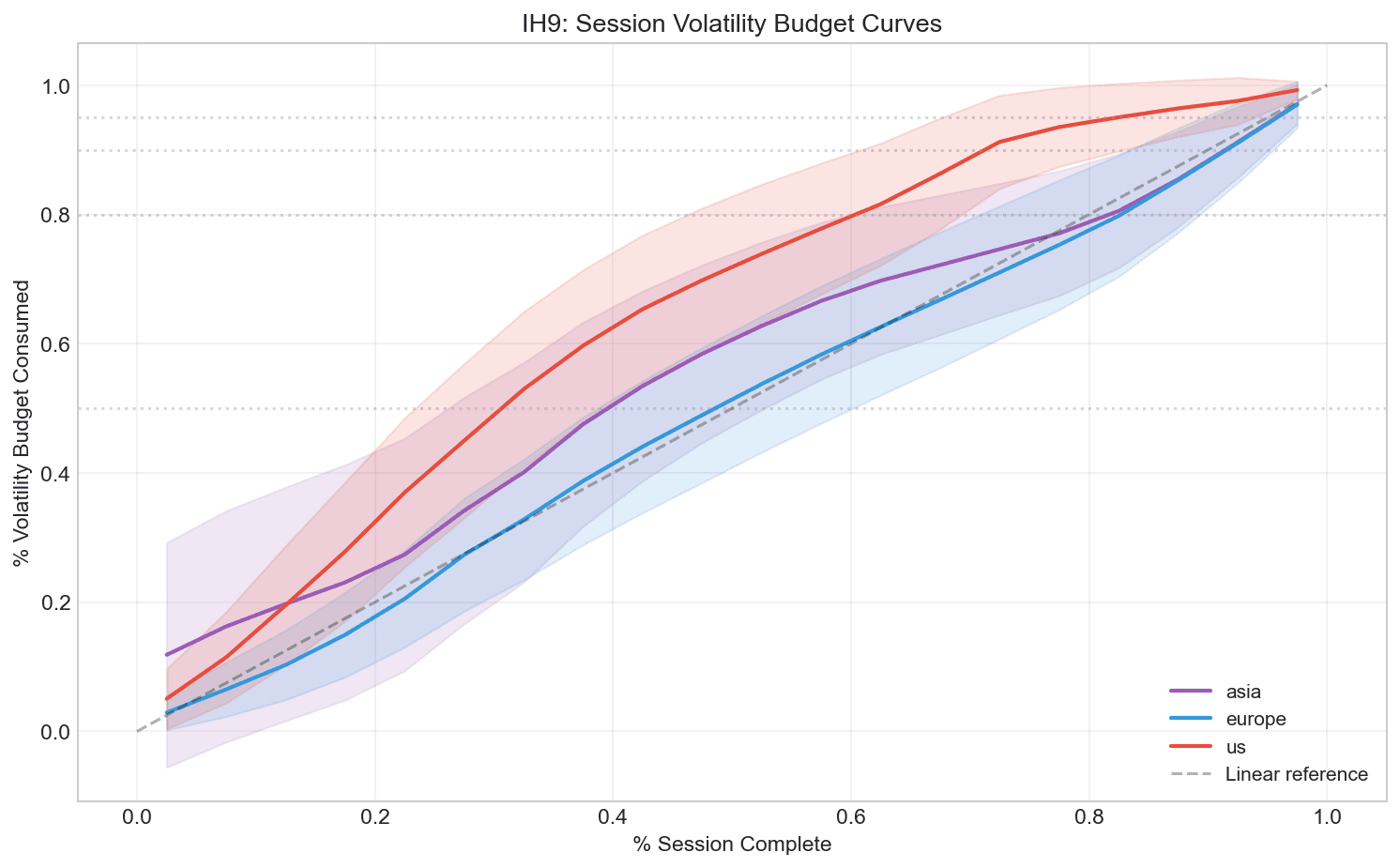

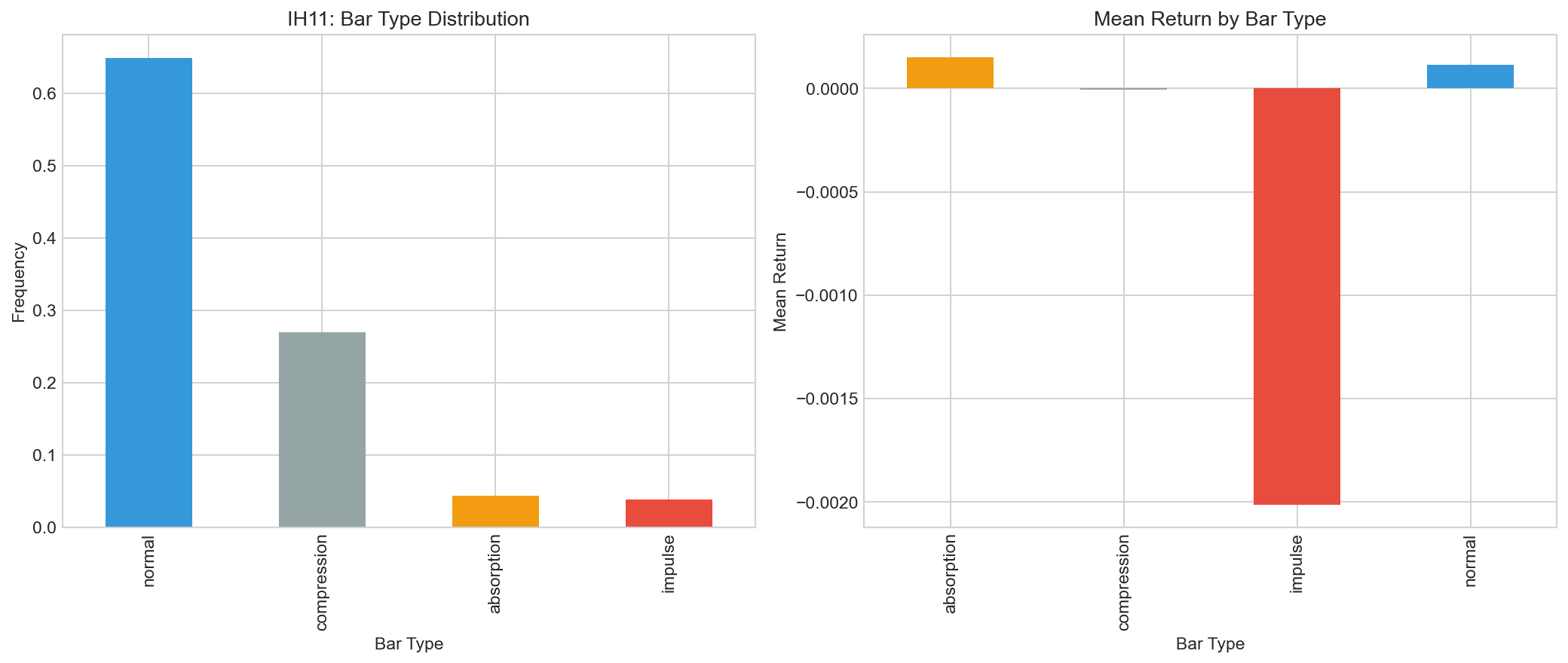

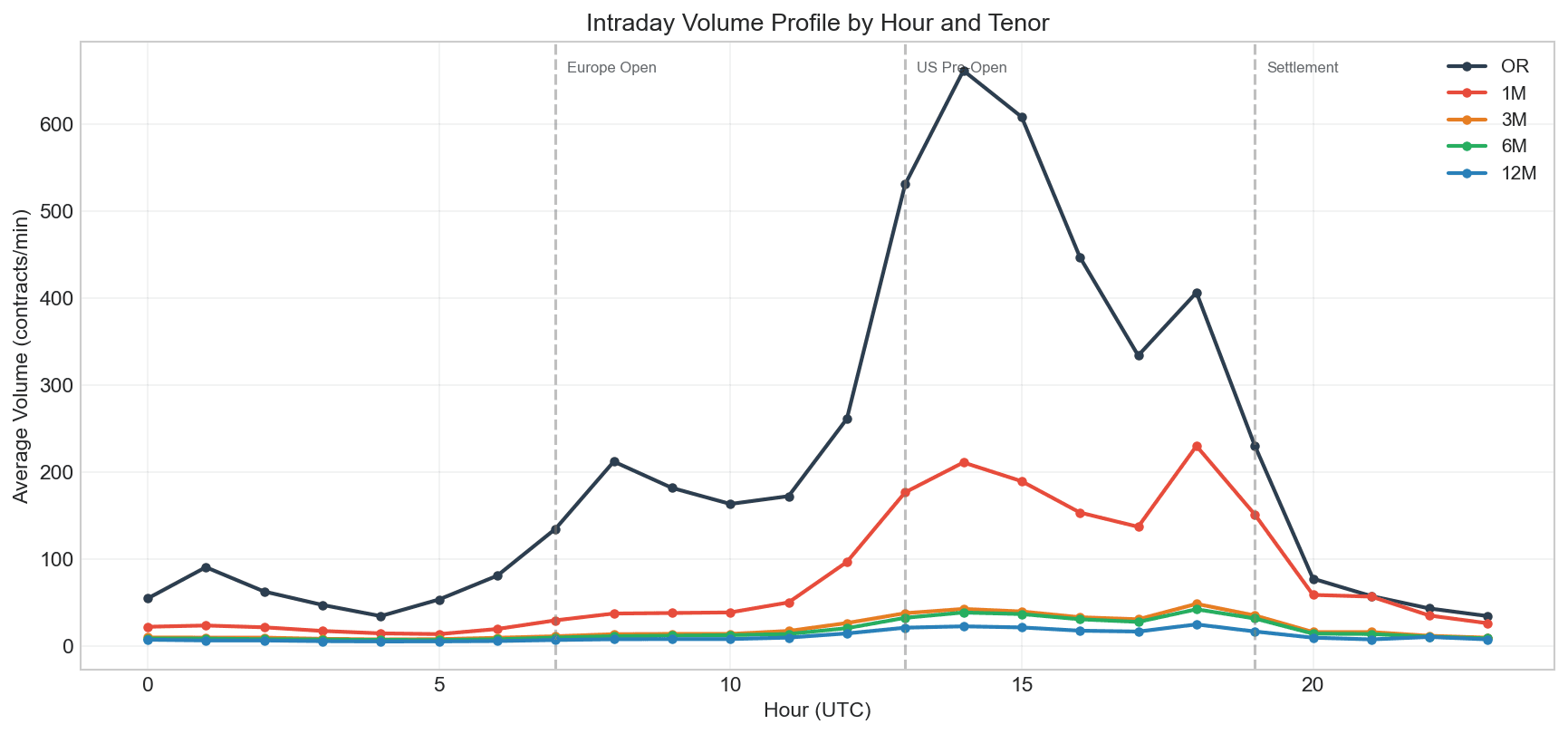

Volatility

3 plotsSession Energy Buildup Curves

Bar Type Distribution

Hourly Volume Profile

Events

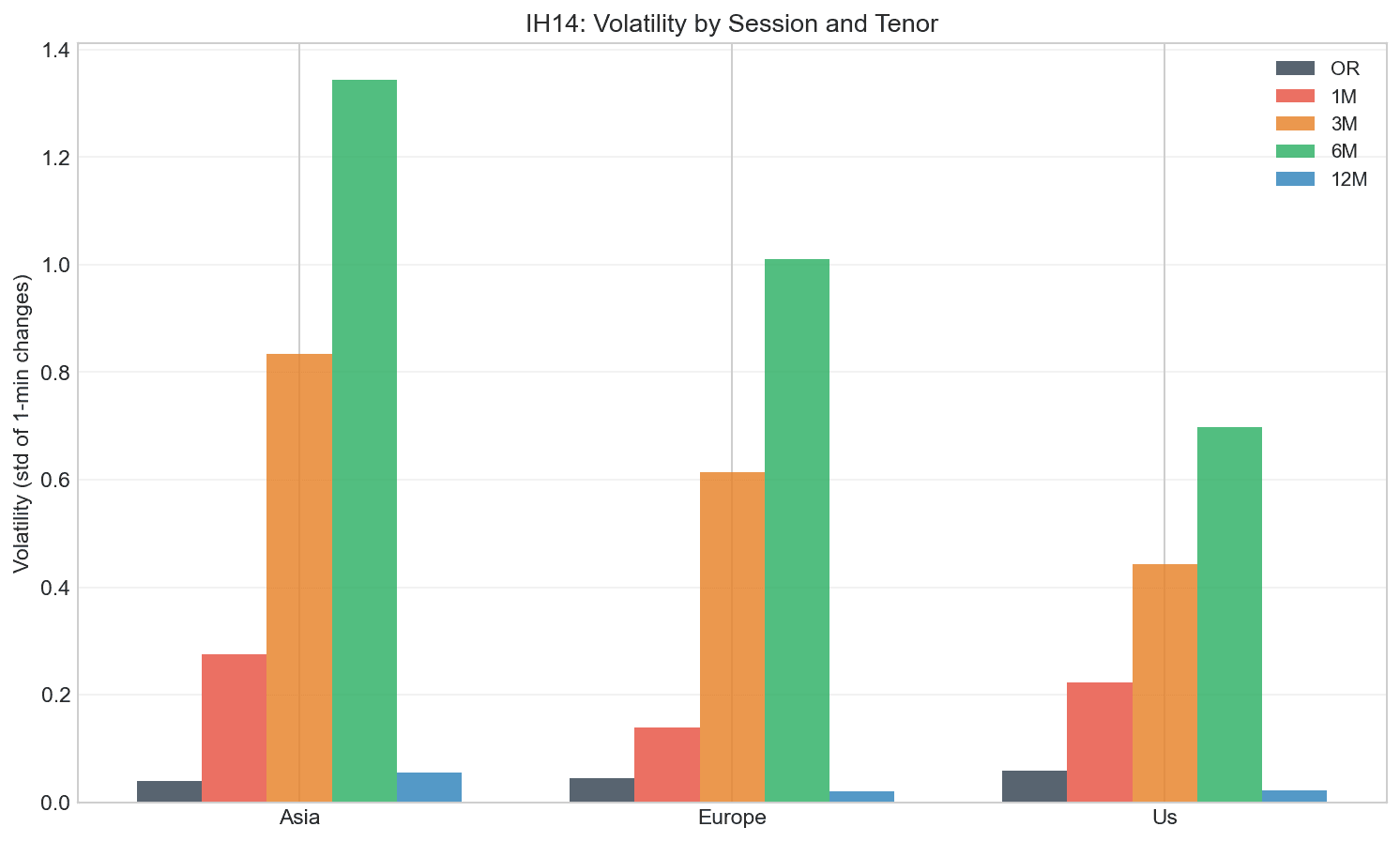

3 plotsSession Volatility Comparison

EIA Volatility Ratio Paradox

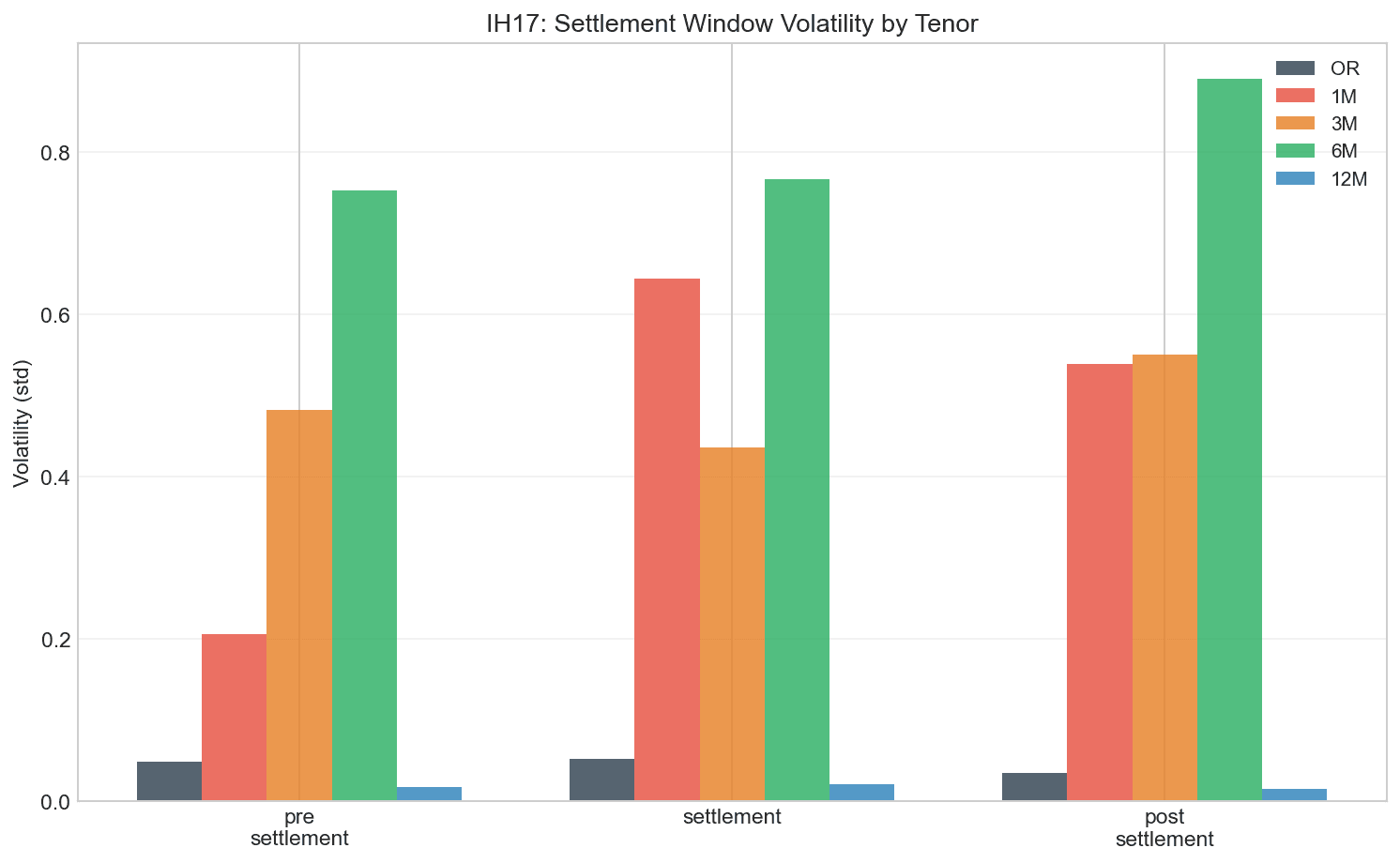

Settlement Window Volatility

Fractal

3 plotsHurst Exponents by Tenor & Timescale

Butterfly AR(1) Decay

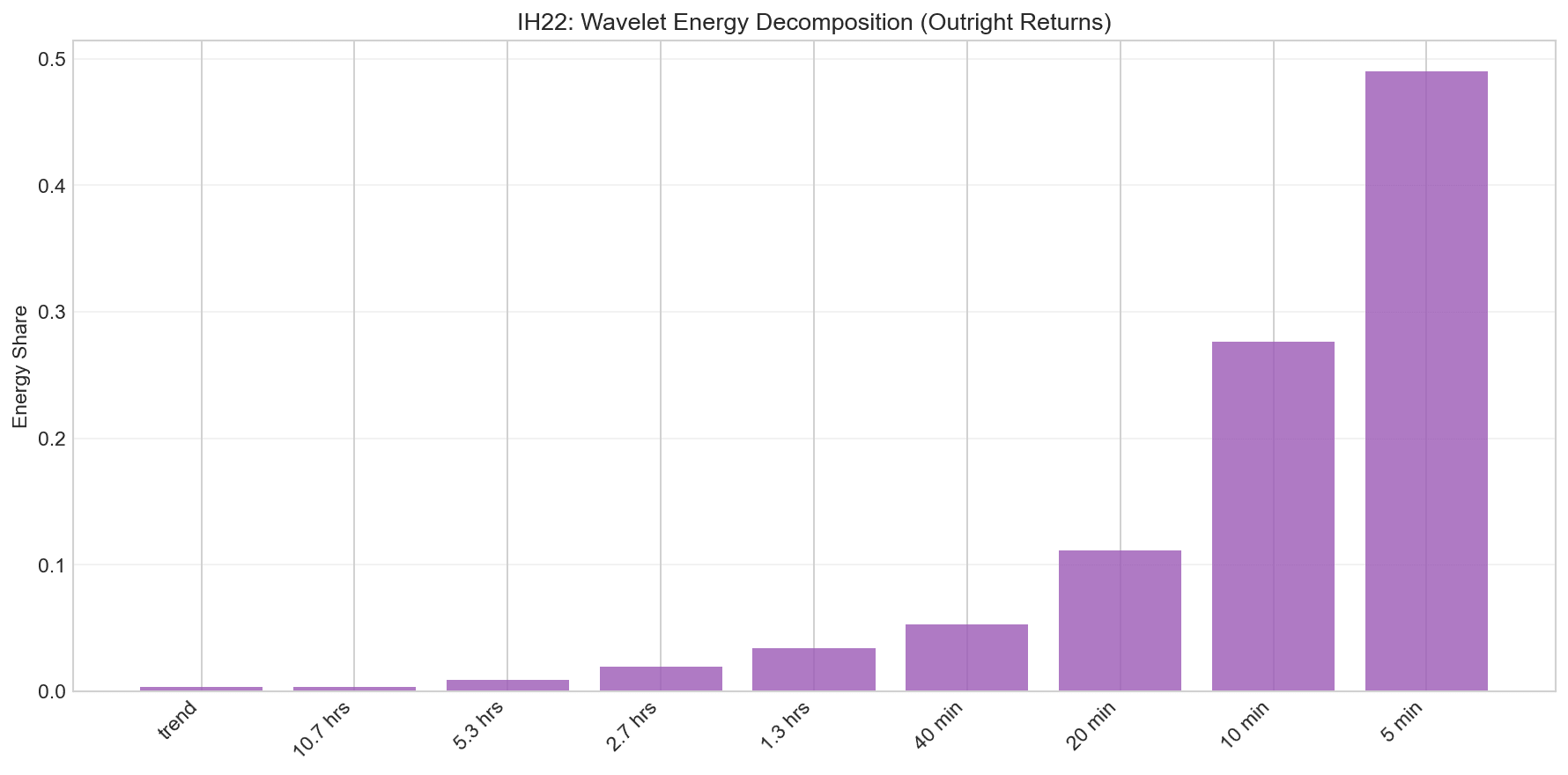

Wavelet Energy Distribution

Advanced

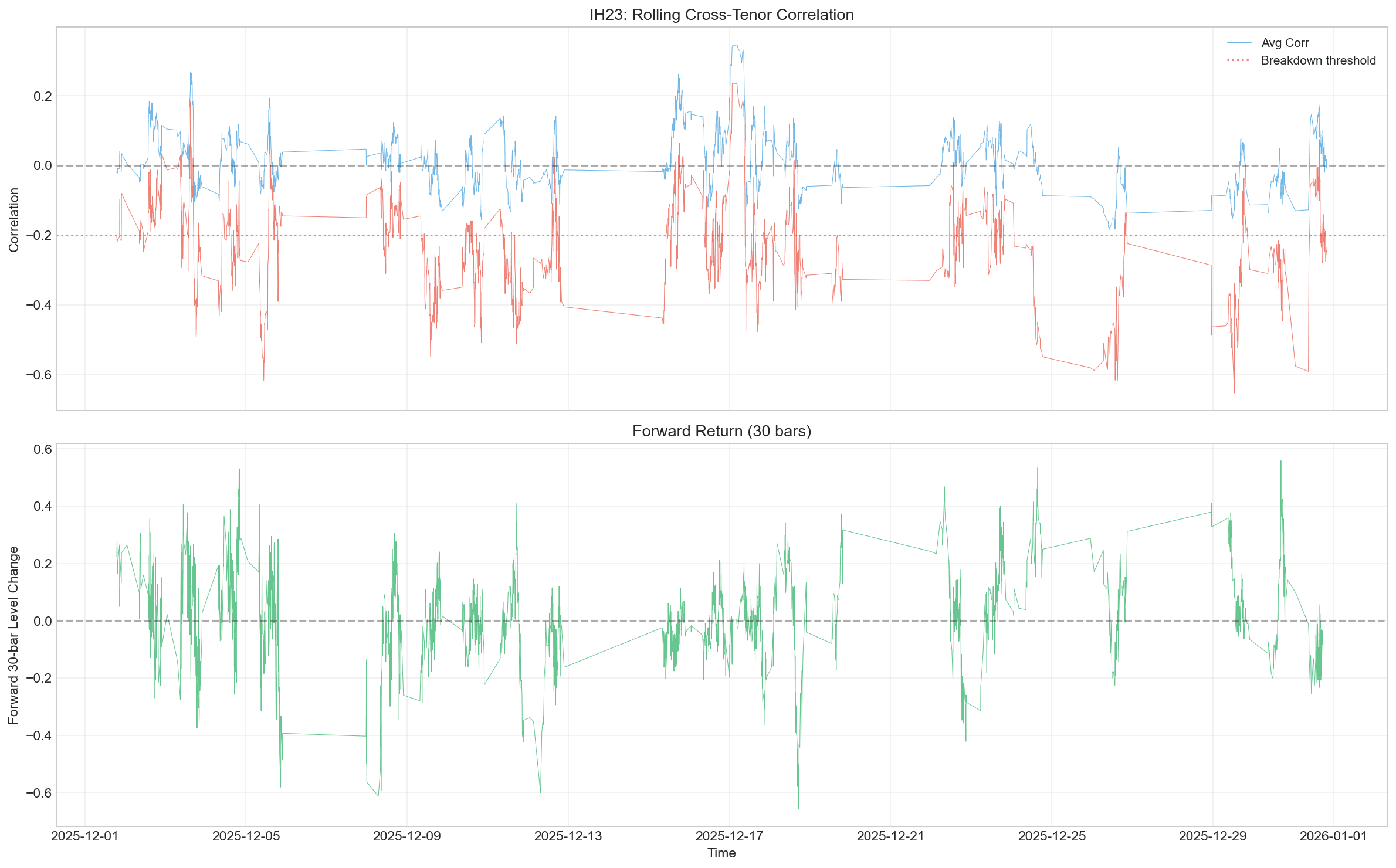

3 plotsCorrelation Breakdown Forward Returns

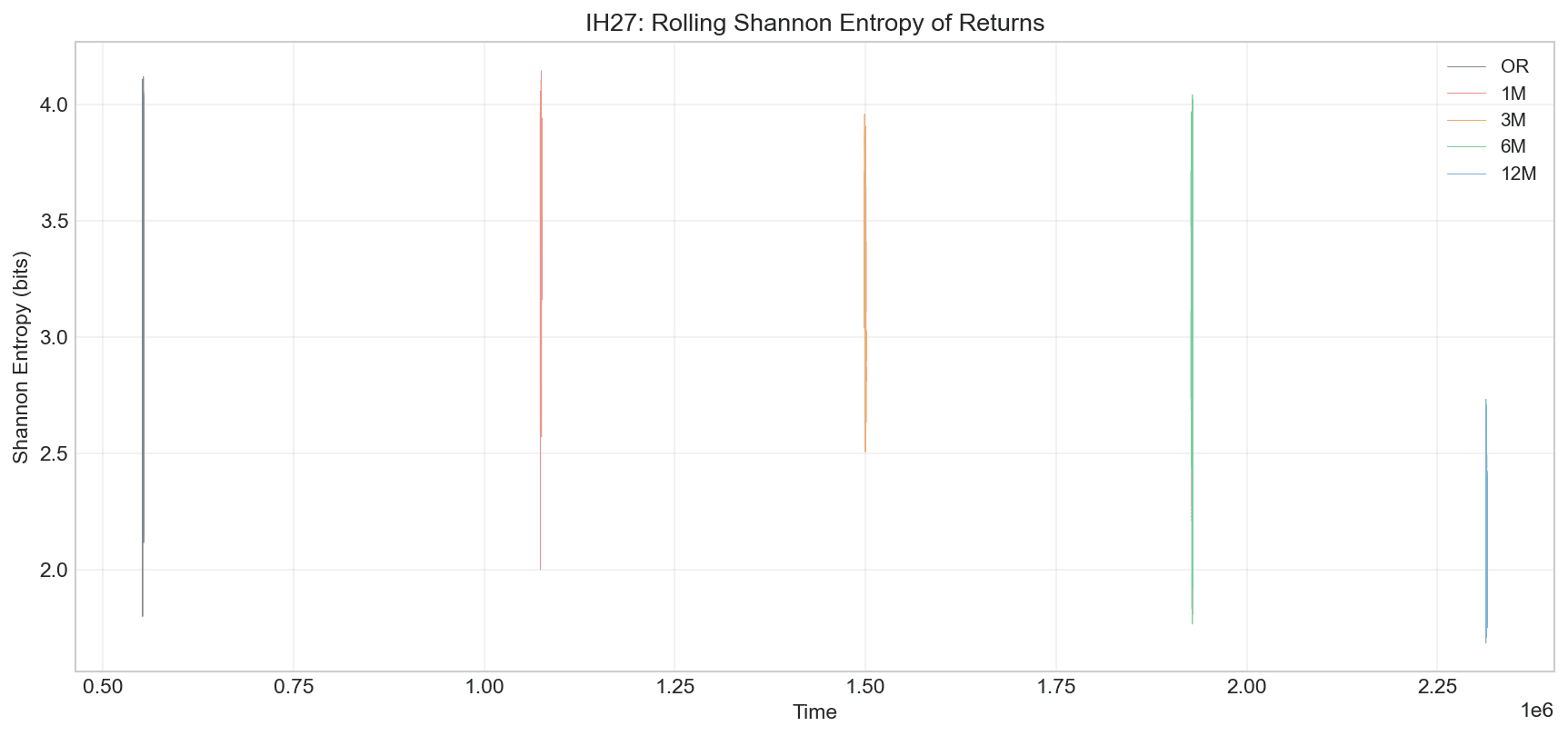

Shannon Entropy Evolution

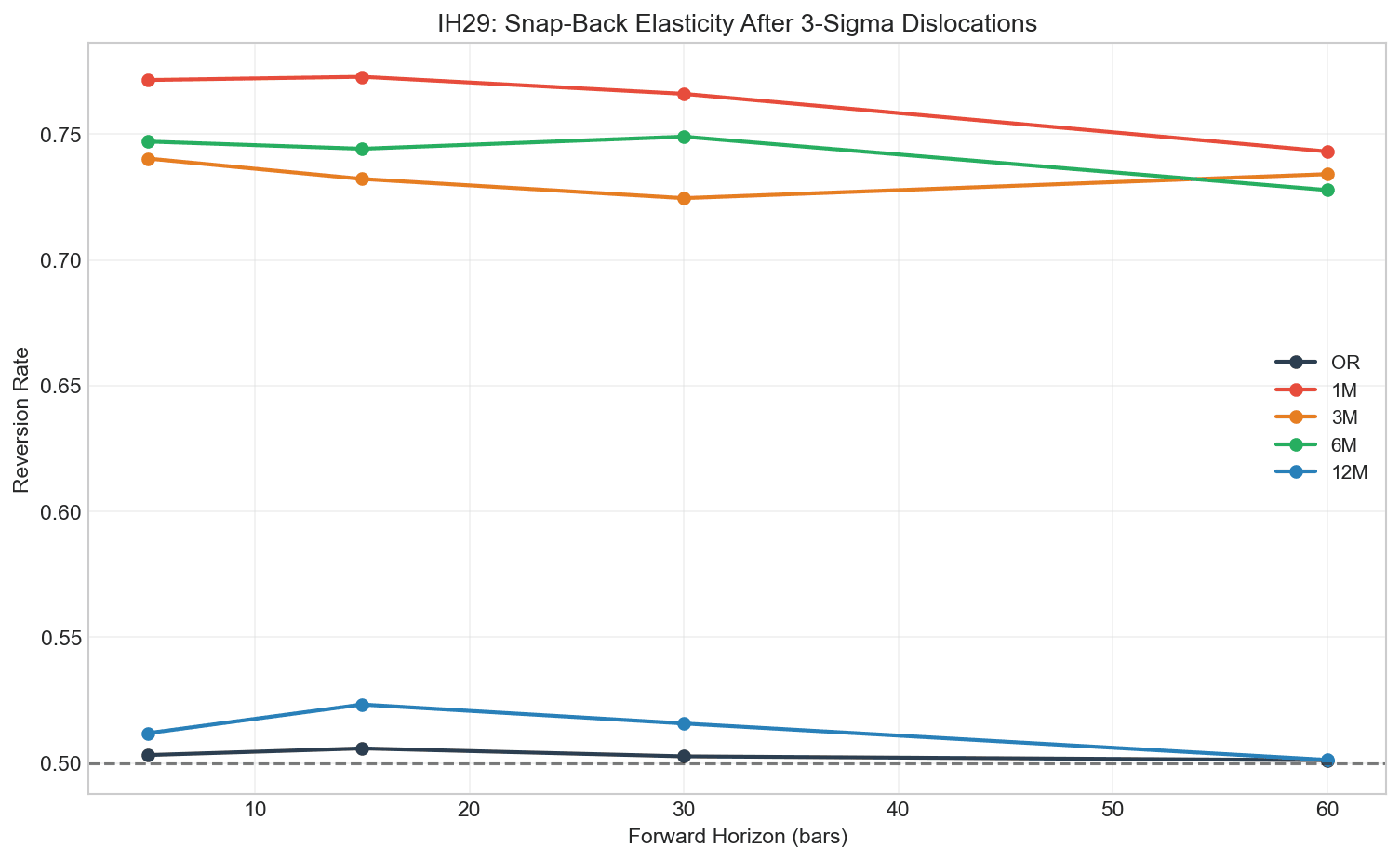

Snap-Back Reversion Rates

Strategies

1 plotsTrade Archetype Comparison

Background

Experience & Education

Quantitative Researcher / Trader

Blueberry Capital | Gurgaon, India

- •Developed ML models for trading crude oil forward curve, achieving portfolio Sharpe ratio of 3.4 through systematic signal generation across multiple contract maturities and term structure regimes

- •Built and deployed 3 live strategies integrating alternative data: EIA weekly petroleum reports, FRED macroeconomic indicators (GDP, industrial production, rates), and proprietary market microstructure features

- •Architected end-to-end execution infrastructure in Python (FastAPI, WebSocket) for automated order generation, risk checks, position management, and real-time P&L monitoring

- •Engineered feature pipelines processing energy fundamentals, forward curve dynamics, inventory surprise signals, and macro regime indicators with ensemble ML (XGBoost, neural networks)

Quantitative Trader

Futures First | Hyderabad, India

- •Developed statistical models for energy futures (crude oil, natural gas, heating oil, RBOB, gasoil) generating alpha across multiple contract maturities

- •Executed algorithmic strategies: event-driven, trend-following, and mid-frequency arbitrage boxes for consistent daily profits

- •Applied regression analysis for hedge ratios across Abu Dhabi crude, Brent, WTI; Monte Carlo stress testing; seasonal analysis for strategy optimization

- •Managed multi-commodity portfolio (intraday to seasonal): mean-reverting, trend-following, arbitrage, inter-product and calendar spread strategies

B.E. in Computer Science

Nagpur University

Nagpur, India | 2018 - 2022

CGPA: 9.2 | Coursework: Machine Learning, Deep Neural Networks, Data Mining, AI

Executive Program in Algorithmic Trading

QuantInsti Quantitative Learning

Mumbai, India | Jan - Jun 2022

Quantitative Trading, ML in Finance, HFT, Risk Management, Derivatives

Certifications

Technical

Skills & Tools

Programming

Quantitative

ML & Methods

Infrastructure

Contact

Let's Connect

Open to quantitative research roles, trading opportunities, and collaboration in systematic strategies